When you’re in the process of applying for a mortgage loan, perhaps to buy your first house, there are a lot of terms thrown around. You might hear vernacular like “closing costs,” “Yield Spread Premiums,” and “Debt-to-Income Ratio” for the first time. There are even plentiful acronyms, like FHA, PMI, and one we’ll talk about today, APR.

When you’re in the process of applying for a mortgage loan, perhaps to buy your first house, there are a lot of terms thrown around. You might hear vernacular like “closing costs,” “Yield Spread Premiums,” and “Debt-to-Income Ratio” for the first time. There are even plentiful acronyms, like FHA, PMI, and one we’ll talk about today, APR.

In fact, APR stands for Annual Percentage Rate, and it is one of the most important numbers for any homeowner and mortgage holder, and yet, it’s one that’s often misunderstood.

Here are ten things you should know about APR – and how understanding it correctly will save you money!

1. First, let’s float a useful definition of Annual Percentage Rate (APR).

An APR is a rate charged for borrowing money in the form of debt (usually with credit cards or mortgages) on an annual basis. But while APR is expressed as a percentage similar to the more common interest rate metric, it also includes fees and costs associated with obtaining the loan. Therefore, APR has been called the “true” cost of the loan, as it includes the annual interest rate and transactional costs you pay.

2. Now, let’s look at how APR differs from a mortgage interest rate. The APR represents the mortgage interest rate PLUS an additional charges, costs, and fees. Therefore, the APR is never lower than the interest rate. An interest rate, however, only shows the annual interest charged on the loan – or the amortized cost of borrowing the money – and never anything else. Therefore, it’s often called the “nominal interest rate.”

The easiest way to think about it is that your interest rate will determine your mortgage payment every month (or credit card payment). But the APR will reflect the total cost of that loan, including what they’re paying to GET that interest rate.

3. What kinds of costs are wrapped into an APR that aren’t reflected in an interest rate:

Of course, any mortgage loan comes with associated fees the borrower must pay to procure the loan. The APR takes into account these costs, too, above and beyond just the interest rate. These costs are all amortized over the life of the loan with the APR, even if they are paid up front by the borrower.

These include:

- Points you pay like discount points

- Mortgage origination fees

- Closing costs

- Mortgage insurance

- The actual nominal interest rate

- Other associated charges

4. What might NOT be included in the APR:

While APR is a great barometer for comparing different loan options side by side, it’s not all-encompassing. That’s because your APR may be missing a few things. Sometimes, lenders don’t include certain items like appraisal fees, credit report fees, and inspections in the APR. Likewise, online lenders have been known to reel in a loan shopping consumer with promises of low APRs, only to later disclose that mortgage insurance costs weren’t included in that first APR.

5. Where can you find your APR?

When we first fill out a mortgage application with you, you’ll quickly receive a Loan Estimate from me. Right on page 1 of this Loan Estimate, you’ll see a section called “Loan Terms” that shows the interest rate. But if we turn to page 3, you’ll see the actual APR of the proposed loan listed.

The APR will also be listed prominently on your loan closing paperwork. Of course, you can ask me about your interest rate or APR any time, and I go over this important information several times with each mortgage applicant.

6. Fixed or variable – the two kinds of APRs:

Since mortgage interest rates can either come as fixed or adjustable, your APR needs to reflect that, too. Therefore, an APR can be fixed or adjustable, too. If your mortgage can adjust, with the payment going up or down, at a certain period, you’ll have an adjustable APR. But if your payment will be exactly the same for the life of the loan (usually 30 years), your APR will be fixed.

7. APR – it’s the law!

Listing the APR is not optional for lenders. In fact, the federal Truth in Lending Act mandates that the APRI is prominently and clearly listed on every loan agreement, as well as the nominal interest rate.

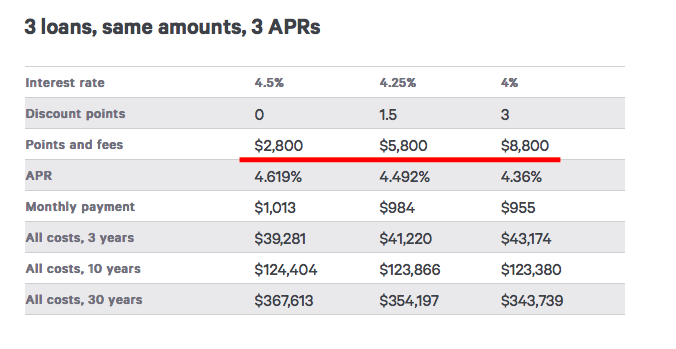

8. Take a look at this example of APRs as presented by a credible and well-known financial website. These interest rates and APRs are for illustration purposes only to educate you about APR and empower you as a consumer, and don’t reflect any actual loan rates being offered.

9. Where APR can be misleading:

Since APR basically amortizes your major costs and fees of obtaining the loan over the 30-year term, it’s only entirely accurate if you keep the loan for that full 30 years. However, when people pay off their mortgage loan – by paying it down and off, or through a sale or refinance, the APR is no longer accurate. In fact, loans with more sizable up-front fees and lower interest rates will have lower APRs, but when you pay your loan off early, that APR will actually be higher.

So think about how long you want to stay in the home (and the loan), as well when you compare APRs. If you have a short-term, adjustable rate loan, or know that a sale or refinance is imminent, then maybe focus on the interest rate and monthly payment more, while still taking into account the APR.

10. Should you look for a loan with a low interest rate or a low APR?

Consider the Annual Percentage Rate a great tool in comparing different loan products and different lenders. If two loans have the same nominal interest rate but one APR is higher, you’re being asked to pay more to obtain that loan.

But a wise consumer will also consider how long they’ll be in the loan, too. A loan with a low interest rate and monthly payment but a slightly higher APR (possible due to Discount Points that bought down that interest rate) may be the best fit, or a lower APR may be best if you have a short-term or adjustable loan or plan on refinancing or selling.

I’ll compare both options with you, and carefully explain the interest rate AND APR on any loans you’re considering! Please contact me if you have any questions about your APR or your mortgage!